When I first heard about the idea of financial independence, it almost sounded too good to be true. How was it possible that people were retiring from their jobs or quitting their jobs to pursue a passion before the traditional retirement age? Currently the full retirement age is 67 (for everyone born after 1960), so how can someone in their 40s or 50s be retired? It turns out that retirement isn’t just a random age at which you can quit your job, but rather it is based on your expected retirement expenses and the amount you have invested, or expect to get via social security and pension. Once you have enough money invested to cover your expected annual expenses (housing, food, healthcare, transportation, entertainment, etc.), then you can retire. In essence, some people have enough invested prior to the the full retirement age, so they have the flexibility to retire early, or continue working knowing that they have the flexibility to quit if/when they want to.

There are a variety of factors to consider when determining how much money you need for retirement, such as your expected expenses, healthcare costs, social security/Medicare benefits, expected pension, and the type of lifestyle that you want to live (frugal, lavish, or somewhere in the middle). A mortgage payment tends to take up a big chunk of people’s paycheck, but if you are living in a paid-off home at retirement, that is one less expense to consider.

One way to calculate your expected retirement savings needed is to use the 4% rule. The 4% rule is designed to have a higher chance of your money lasting for at least 30 years. To calculate how much you need for retirement using the 4% rule, multiply what annual income you’d like to have in retirement by 25, and you will get your retirement savings target.

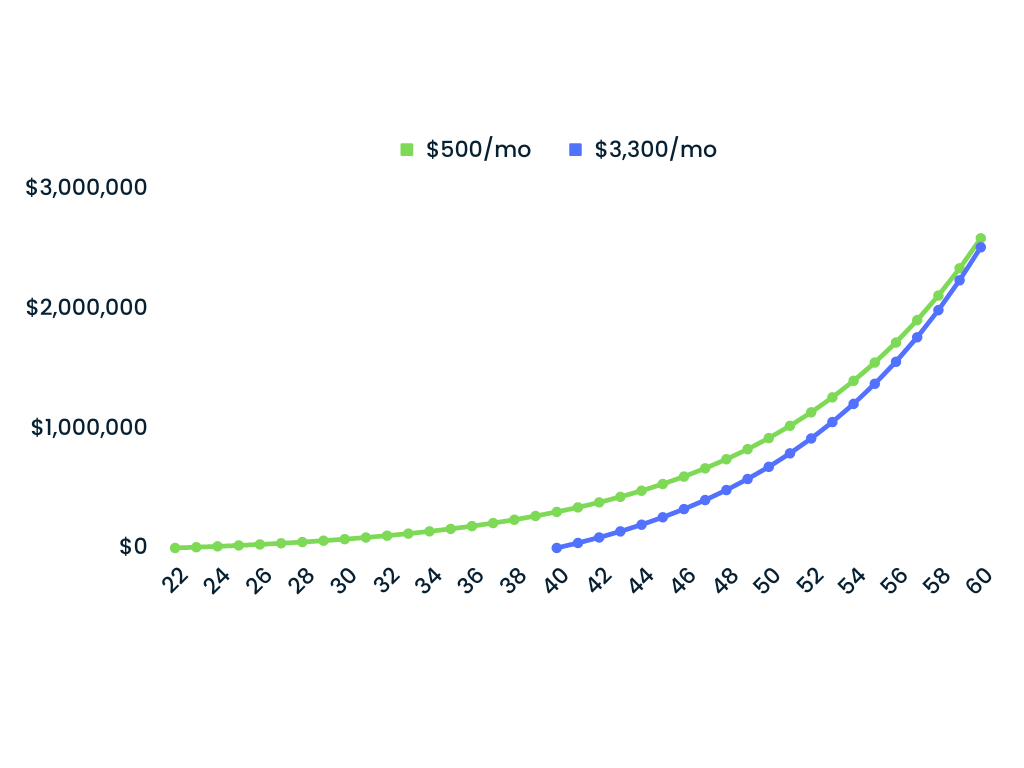

For example, if you want an income of $100,000/year in retirement, $100,000 multiplied by 25 equals $2.5 million. The ChooseFI website has an awesome calculator that can help you estimate how much you need. The idea of having $2.5 million saved or invested sounds overwhelming but I love that this calculator shows you that this is absolutely doable. If you start investing $500 per month at age 22, around what a car payment may be, and you add just $500 per month, every month, until you are 60, with a 10% return in the stock market, you would have over $2.5 million dollars at age 60. (https://www.choosefi.com/retirement-projection-calculator/)

I know starting to save for retirement at 22 doesn’t sound fun. There are probably a million other things that you would rather spend your money on, BUT I want to point out the significance of investing over a long period of time and the power of investments compounding over decades. Say you still want to retire at 60 with $2.5 million, but you wait until you are 40 to start investing – you would need to invest $3,300 per month, every month, until you are 60 to hit that same $2.5 million. Just by starting at 22 years old, rather than 40, you are able to retire with the same amount at 60, but by contributing $500 per month, rather than $3,300 per month. Once you start saving a certain amount per month, it becomes a habit and you don’t even see or think about that money anymore. Out of sight, out of mind!

Graph showing the power of compound interest and investing over a long period of time. The green and blue lines both end at ~$2.5 million at age 60 but the person who invested $500/month starting at age 22 (GREEN) invested a total of $228k and the person who invested $3,300/month since age 40 (BLUE) invested a total of $792k. Realistically, how many people even have $3,300/month to invest into a retirement fund. This scenario is not practical for most people but I think it illustrate how important starting early is!

The really cool thing about financial independence (and personal finance in general) is that it is so personal and every person is on a different journey. Online calculators can certainly help you estimate how much your investments could be worth in the future but only you can take a good, honest look at your finances and figure out how much you can invest. There are people in the financial independence community who had very high-paying software engineering jobs who lived extremely frugally and invested thousands of dollars per month to become financially independent quickly and there are stories of blue-collar workers who invested comparatively less per month, but by investing consistently and over a long period of time, were able to also become financially independent.

If all of this is brand new to you, but it sounds even slightly intriguing, I recommend taking time to reflect on your current situation and think about your ideal financial situation. If you absolutely love working and don’t mind working until the full retirement age, then maybe financial independence is not for you, but if that is not the case, the concept of financial independence is worth looking into more!

I am super passionate about this topic so if you have any questions or concerns, please leave a comment and I’d love to chat with you!